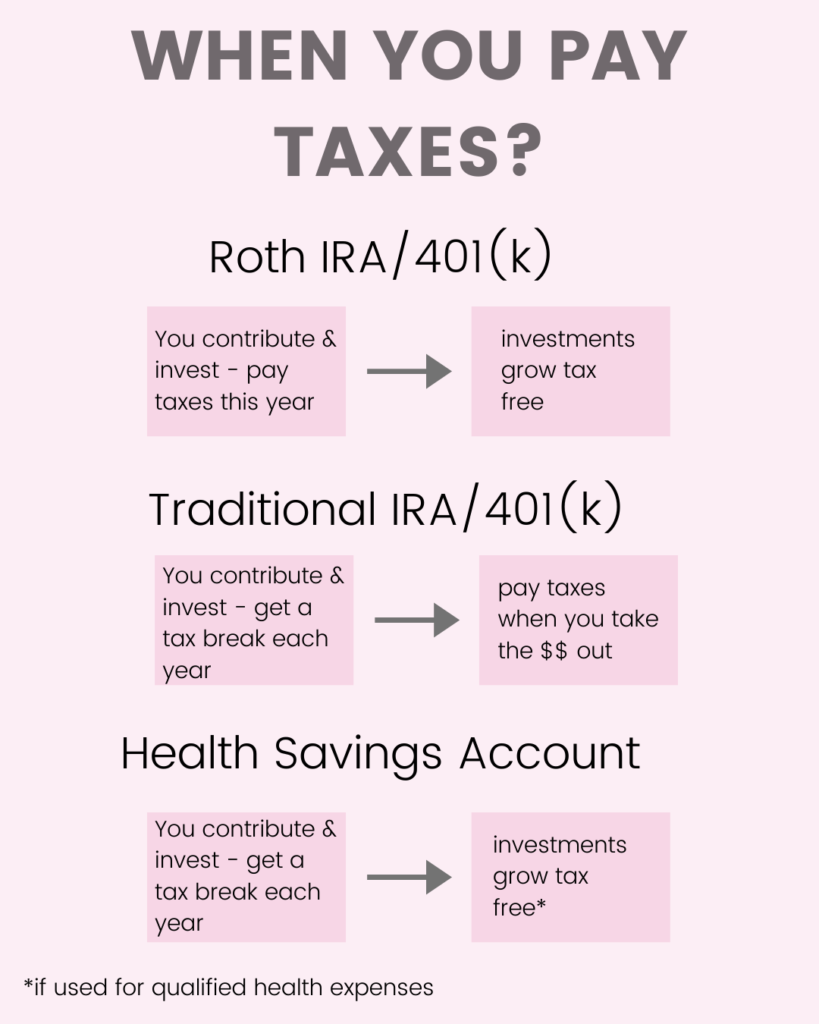

HSA accounts are meant for healthcare-related expenses, but once you retire, you can use the funds for any purpose without penalty. Before you turn 65, if you withdraw funds for anything besides healthcare expenses, you’ll pay a 20% penalty plus taxes. After age 65, you can withdraw them. If you use them for anything besides healthcare expenses, you’ll just pay the income tax on the funds.

If you are like me and want to retire early, here’s my plan for using my HSA to retire early.

Pay for current medical expenses out of pocket

I want to take advantage of compound interest for as long as I can on my HSA investments so I am funding my health care expenses out of pocket that doesn’t get covered by insurance. As I am younger, my health related expenses are relatively lower, but I assume as I get older this will get more expensive.

Contribute the maximum every year

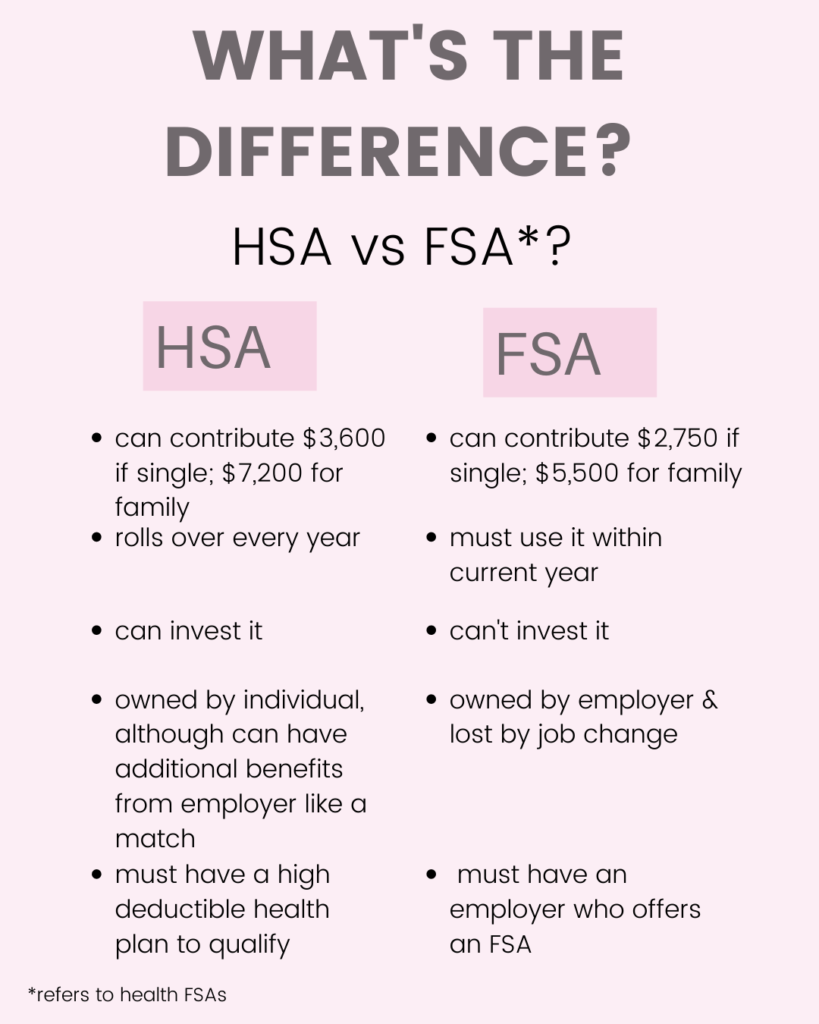

As someone filing taxes single, I am eligible to contribute up to $3,600 annually into my HSA account in total. As an incentive to use it, my employer matches $400 per year so I can contribute up to $3,200 and get $400 added to my account free.

Invest in low cost index funds

Within my HSA, I keep a consistent strategy of investing in low cost index funds. My HSA provider gives me the option to invest in Vanguard’s mutual funds so I select a Total Stock Market Index Fund with an expense ratio of 0.04%. This allows me to avoid losing too much of my investment growth too fees and take advantage of as much compound interest as I can.

Use my HSA penalty free after age 65

After the age of 65, you can withdraw from your Health Savings Account penalty free. On average, it will cost you anywhere from $100,000 to $300,000+ on health related expenses in retirement. This will depend on a number of factors but most closely tied to how healthy you are personally. Given this, I don’t think I will have an issue spending my HSA funds on health care expenses. However, if I do decide to use this money on non-health related expenses, I would not have to pay any penalties after the age of 65 and I will just be subject to my income tax rate at that point in time.