Before we get into how to grow your score, it is important to know how it is determined. Companies use figures in your credit report to create your credit score. The 3 major credit reporting agencies are Equifax, Experian and TransUnion.

Most lenders typically use FICO score, a 3-digit number based on the information in your credit reports

A few factors come into play when creating your score.

They include inquiries (how often you’re applying for new credit), your payment history, your length of credit history, your credit utilization ratio (how much credit you use vs. your credit limit) and your credit mix (installment vs. revolving credit).

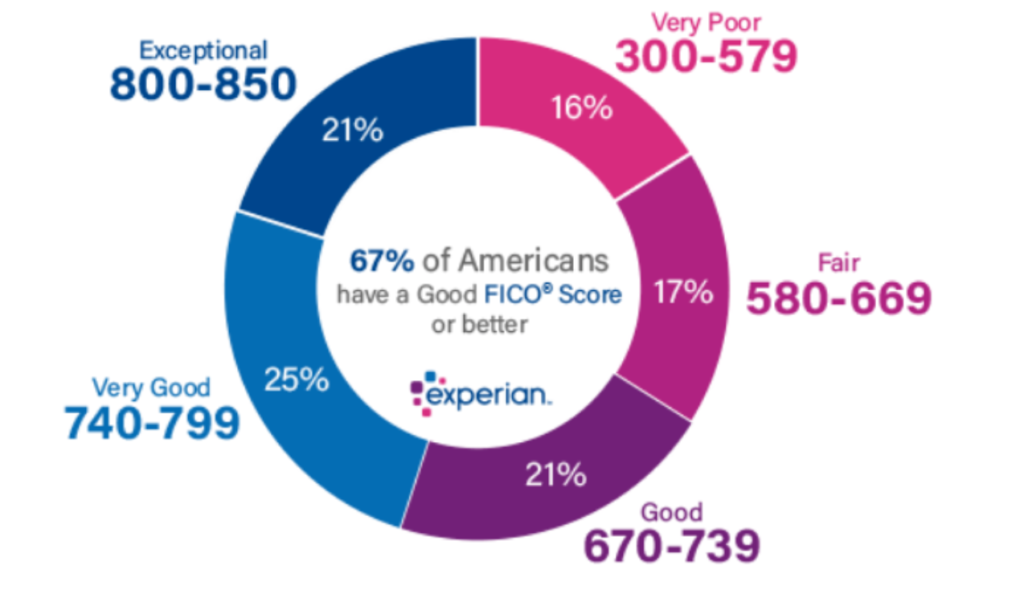

Based on these factors, your FICO score can range from 300-850.

300 – 579 Very poor

580 – 669 Fair

670 – 739 Good

740 – 799 Very good

800 – 850 Exceptional